Credit Scores have us in a chokehold, but why?

For many people, credit scores feel like the be-all and end-all. They’re seen as the magic number that decides whether or not you can buy a home, get a car or fund essential home improvements. For others, checking their score has become a constant merry-go-round – thanks to the gamification created by companies using data provided by credit reference agencies (CRAs).

But here’s the real question: why are companies gamifying the process?

Because it makes them money… a lot of money.

Our obsession with credit scores keeps us checking them and encourages us to take out credit. And every time you do, these companies often get a financial kickback from banks and credit card companies.

To pull back the curtain on this industry, we spoke to someone who worked at a credit reference agency to get an insider’s view.

“Credit scores are made up”

“I worked at a CRA for three years (2017-2020) and it really opened my eyes to the absolute money making industry that is your credit score. I can’t believe I fell for it for years myself.

I was actually told by the company directors that credit scores are made up. When you look at the different score providers out there, you start to realise how true this is as each one has a different score total… I mean how ridiculous! No-one actually knows how a lender will view your report and score you.

Scores are basically their best guess on how a lender might look at you.”

What really goes into a lending decision?

It’s not all about a single number. Lenders consider a whole range of factors, including:

- Affordability

- Dependants

- The current economic climate

- Employment status (self-employed vs. employed)

- Homeownership status

- The lender’s own appetite and capacity to lend

The automated “yes” or “no” you see when applying for credit makes it seem like it all comes down to a score, but in reality, every lender has their own criteria. That’s something credit score providers will never fully know.

Are credit scores important?

Yes and no.

It is important to know what’s on your credit report and make sure the information held about you is correct. If a lender is reporting inaccurate data, or if old financial relationships are still attached to your file, you’ll want to get those removed.

But the score itself is completely irrelevant.

It is just a money making scheme by the agencies to get you to purchase a product (i.e. loan or credit card) that they get an affiliate income from.

Instead of obsessing over your score, focus on what really builds financial confidence: like tracking your net worth so you can measure progress on your own terms.

How can you actually see what’s on your report?

You have the right to access your credit report directly from the three main UK agencies:

- Experian

- Equifax

- TransUnion

All other companies simply access your data and then ‘reveal’ it to you either as a pretty looking score which tempts you to purchase an affiliate product or as part of a premium subscription trap (e.g. free for the first 30 days then create a maze for you to navigate in order to cancel in the hope that you’ll forget about the monthly payment).

The smarter move is to go directly to the agencies. If you spot an error, you can raise it with the lender or the CRA to have it fixed.

What if there’s a dispute on your report?

If a lender doesn’t agree that they’re at fault, you may have to escalate the issue with them directly or go through the Financial Ombudsman.

It’s also worth knowing that updates to your report (like new accounts, closed accounts, or corrections) can take up to two months to show. And each CRA handles data differently. For example:

- Equifax: Data stays for up to six years on an open account, then six years after closure.

- TransUnion: Data is removed after six years, whether the account is open or closed.

This means your report could look quite different depending on which agency a lender uses — and not all lenders report to all CRAs.

Basically, don’t stress about the score. Focus on the details in your report and make sure they’re accurate.

You can’t do anything more about the score as it is all made up anyway.

How can you improve your credit worthiness?

If you want to strengthen your position with lenders, focus on the things you can control:

- Get on the electoral roll

- Make sure any expired financial connections are removed (ex-partners or housemates you no longer live with or share accounts with – this is a biggie because as long as they stay on your report, and vice versa they will affect a lending decision about you)

- Check that your lenders are reporting your history correctly (and challenge any mistakes).

And remember: changes can take a couple of months to show. There’s no need to check your report every few weeks.

Want something more practical to focus on instead? Try building an emergency fund or using sinking funds to get ahead financially – both will make a much bigger difference to your long-term money confidence than a made-up score ever could.

Final thoughts

Credit scores might feel like the key to everything, but the truth is: they’re a money-making tool for many companies, not a reflection of your financial worth.

What matters most is making sure your report is accurate and reflects your real situation. That’s what lenders really care about.

So the next time you feel tempted to obsess over your “score”? Step away from the screen. Your financial wellbeing isn’t defined by a number someone else made up.

The Great Lock In: Debt Edition

How to Stop Using Buy Now Pay Later

Lorna Luxe in shock debt confession

Why Buy Now Pay Later Targets Women

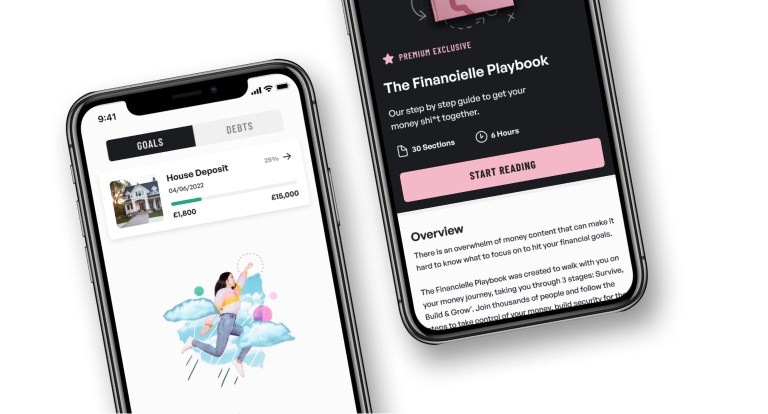

Download the Financielle app now

Never be overwhelmed by money again.