We know that buying a car outright can be a financial stretch, but if there’s one place we can offer big sister money advice, it’s the world of car finance and its hidden pitfalls.

As tempting as these monthly payments can feel when the dopamine hit is dangling like a carrot, the financial commitment can soon turn into a burden when you want to get your money $h*t together.

Before we look at why we don’t love car finance, check out the options available to you in the UK (with a handy Financielle warning attached).

1. PCP – Personal Contract Purchase

Think of this as rent-to-own… if you want to.

- How it works: You pay a deposit, then monthly payments for a few years. At the end, you can either:

- Pay a “balloon payment” to keep the car,

- Hand it back, or

- Trade it in for a new one.

Financielle Warning Watch out, that final payment can be chunky.

2. HP – Hire Purchase

More like a slow-burn purchase plan.

- How it works: Pay a deposit, then fixed monthly payments. When you’ve paid it all off you own the car.

Financielle warning Monthly payments are usually higher than PCP because you’re covering the full cost.

3. PCH – Personal Contract Hire

This is leasing, pure and simple.

- How it works: Pay a deposit, then fixed monthly payments to rent the car. At the end, you give it back, no option to buy.

Financielle warning You’re paying for use, not ownership.

4. Personal Loan

Old-school and flexible.

- How it works: Borrow the money from a bank or lender, buy the car outright, then repay the loan in installments.

Financielle warning Interest rates depend on your credit score.

Why we don’t love it

A shiny new car can feel like freedom on four wheels. But if you’re not careful, the way you finance it, plus how quickly it loses value can mean you end up paying far more than it’s actually worth.

Let’s break down why that happens and how to avoid it.

1. Depreciation: Your Car’s “Silent Cost”

Depreciation is how much value your car loses over time. And it starts the moment you drive it off the forecourt.

- Brand new cars can lose 20–30% of their value in the first year alone.

- By year three, many are worth less than half their original price.

If your monthly finance payments are based on the full showroom value, but the car’s value drops fast, you’re at risk of overpaying.

2. Negative Equity: Owing More Than It’s Worth

This is when the finance balance left on your car loan is more than the car’s market value.

Example:

You buy a £25,000 car on finance. After two years, you’ve paid off £8,000 but the car’s value has dropped to £14,000. You still owe £17,000, meaning you’d need to find £3,000 just to sell or trade it in.

3. High Interest = Higher Total Cost

Even if the monthly payments seem manageable, interest can push the total price you pay way beyond the sticker price, especially with longer finance terms.

A low deposit + long term = smaller monthly payments but a bigger final bill.

That’s why Financielle advocates saving up to buy a car, outright, in cash. Saving for a car this way means you won’t have a top of the range Audi or BMW – who wants to blow £40,000 in cash on a car? But you will buy a car that fits in your budget (no lifestyle creep here).

Check out our blog here on how to own a car outright with no financial hangover.

The Great Lock In: Debt Edition

How to Stop Using Buy Now Pay Later

Lorna Luxe in shock debt confession

Why Buy Now Pay Later Targets Women

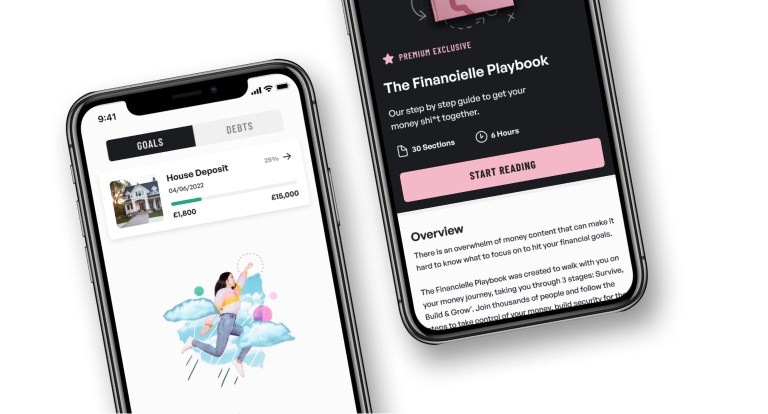

Download the Financielle app now

Never be overwhelmed by money again.